If you’re an employer, you can’t just be on your merry way after paying your employees. You also need to account for payroll expenses in your books. This is where payroll accounting comes into play. To ensure youraccounting books准确,了解如何记录工资交易。

什么是薪资会计?

工资单会计是录制您的书籍中的所有工资交易。作为企业所有者,您将使用薪资日记帐条目记录您的书中的薪资费用。

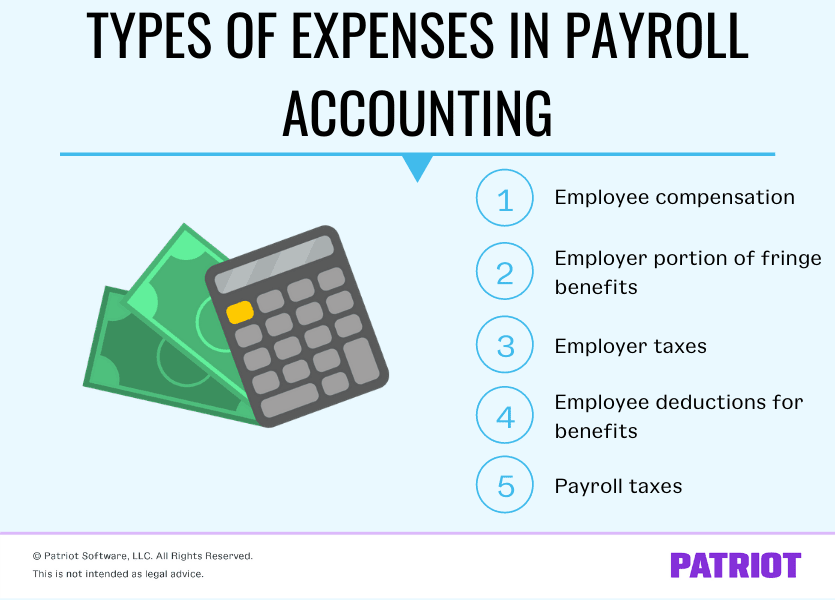

工资记录日记条目属于薪资账户,是您的一部分总帐。记录您的薪资账户中的以下费用:

- 员工赔偿: Salaries, wages, paid time off (PTO), bonuses, commissions, and other taxable income reported on Form W-2.

- 工资税: Federal income, Social Security, Medicare, and applicable state or local income taxes withheld from employee wages.

- 雇主税:社会保障和医疗保险税的雇主匹配,以及联邦和州失业税

- 雇主部分fringe benefits:健康保险,人寿保险,教育援助等

- Employee deductions for benefits: Health insurance, retirement plan, etc.

- Other deductions: Child support, spousal support, outstanding tax liabilities, etc.

工资核算会计有助于您跟踪员工赔偿和其他工资费用。薪资会计为您提供了准确的费用快照。

要清楚地了解贵公司的财务并保持符合要求,请保持您的薪资会计到最新情况。

借记和学分:RECAP

您需要在会计书籍中记录所有工资交易。但在你做到之前,了解使用的基础知识借记和学分在会计中。所以,让我们回到基础知识。

借记和信用是相同但相反的条目。例如,如果信用额度增加帐户,您将使用借记卡增加相反的账户。

借记增加资产和费用账户并减少股权,责任和收入账户。另一方面,信用增加股权,责任和收入账户,减少资产和费用账户。请查看每个帐户类型的借记和信用方式如何影响:

当谈到薪金核算,你一般use费用,责任和资产accounts. Here are a few examples of different types of accounts in payroll accounting:

- 总工资:费用

- 检查:资产

- FICA纳税应付:责任

花费在运营期间,您的业务是您的业务。当您支付员工时,您会增加费用帐户,因为您正在支付它们。

Liabilitiesare amounts you owe. Increase the liability account because, as employees earn wages, you owe more.

Assets是您的企业拥有的价值项目。当您支付员工时,减少您的资产账户以反映现金的减少。

As you do your payroll accounting, record debits and credits in the ledger. Whether you debit or credit a payroll entry depends on the type of transaction made. The debits and credits in your books should always equal each other.

Types of payroll accounting entries

When recording payroll in your books, there are three types of journal entries for payroll accounting that you should know about:

- Initial recording

- 累计工资

- 手动付款

You must handle each type of payroll accounting entry differently. Typically, you work with initial recording entries. Let’s take a look at how each payroll entry compares…

Initial recording

初始录音,也称为始发条目,是薪资会计的主要条目。这是您录制的第一个显示事务。

对于这些条目,记录您的员工赚取的员工和所有扣缴义。此外,包括您欠政府的就业税。

累计工资

Record accrued wages at the end of each accounting period. These entries show the amount of wages you owe to employees that have not yet been paid. After you pay the wages, reverse the entries in your ledger to account for the payment.

手动付款

手动付款偶尔出现在薪资会计中。当您必须调整员工支付或员工终端时,请使用这些条目。

How to do payroll accounting: 7 steps

乍一看,工资核算可能是可怕的。但是,如果您遵循这七个步骤,您可以学习如何轻松地解释薪资。

1.设置薪资账户

如果您还没有,请在您的工资单账户中设置帐户图表(COA)。薪资账户包括费用和负债的混合。以下是薪资账户的一些例子:

- Gross wage expense

- 员工FICA税款应付

- 联邦所得税应付

- 国家所得税应付

- Wages payable

- 员工健康保险应付

- 休假应付

根据您的业务和员工,您可能有额外的薪资账户。

2.计算税收和其他扣除

Calculate taxes and deductions to find out how much you need to withhold from employee wages and contribute as an employer.

税收因员工而有所不同,您的业务位于您的业务。在计算任何税收之前,请刷新状态和当地薪资法。

Hold it!Consider usingpayroll software简化计算税收和扣除的过程。Payroll软件为您处理税收计算,为您提供更多时间来回馈您的业务。

3. Gather payroll reports

如果您决定使用软件运行薪资,请收集报告以获取薪资交易的故障。您可以收集以下报告和文档以使工资单和工资税的录制条目更容易:

- 工资单册: Includes all payroll transactions during a certain period of time, employee names, pay dates, payment amounts, etc.

- 工资单tax report: Shows a breakdown of the taxes you withheld from employee wages, plus taxes you owe as an employer.

您还可能需要提取扣除,捐款和其他福利的报告。

4.记录薪资费用

在您获取有关会计中记录薪资条目的信息后,请转到您的书籍以获得破解。

首先,首先,记录书籍中的工资费用。这包括您在会计期间支付的任何东西(例如,工资,工资等)。

Because they are paid amounts, increase the expense account. As a reminder, expenses increase with debits. Debit the wages, salaries, and company payroll taxes you paid. This will increase your expenses for the period.

When you record payroll, you generally debit Gross Wage Expense and credit all of the liability accounts.

5. Record payables

接下来,记录您欠款但尚未支付的金额的条目。这些金额是负债或应付款项。

Because you owe payroll amounts, you gain liabilities. Liabilities increase with credits. Credit the FICA tax payable, federal income withholding payable, state income withholding payable, and any other withholdings on employee paychecks. Doing so increases your payroll liabilities.

6.仔细检查您的记录

在输入费用和应付款项后,请仔细检查您的记录以获得准确性。

比较您在您的薪资报告中输入的信息。并确保您的借记等于您的学分。如果您的书籍不平衡,请追溯您的步骤以找到您的会计错误并修复它。

7. Transition accounting periods

您最终支付给员工和政府机构的金额。付费负债不再应付。

When you switch accounting periods, make additional journal entries to reduce the cash account and eliminate the liability account balance. Decrease the liability account by debiting the payable entries in your books.

当您偿还金额时,您的资产(例如,现金)减少。要展示资产减少,请为合适的资产账户(如您的现金账户)的减少。

薪资核算示例

了解工资核算可能需要时间。但随着一点练习,您将成为录制工资核算期刊条目的Allstar。要开始,让我们来看看工资记录进入榜样,我们吗?

日记帐分录#1

说你有一名员工在薪水中。您的第一个条目显示您的员工的工资总额,扣缴薪酬税,扣除和净薪酬。它包括以下内容:

- 工资总额

- 员工FICA税款应付

- 联邦所得税应付

- 国家所得税应付

- 员工健康保险应付

- 薪水应付(亦称员工的净工资)

总工资是一项费用,随着借记表决增加。其余的帐户是负债。信用您的负债。这是您的第一个日记帐分录的样子:

| 日期 | 帐户 | 借方 | 信用 |

|---|---|---|---|

| XX/XX/XXXX | 工资总额 | 1,000 | |

| Employee FICA Tax Payable | 76.50. | ||

| Federal Income Tax Payable | 70 | ||

| 国家所得税应付 | 30 | ||

| Employee Health Insurance Payable | 25 | ||

| 薪资应付 | 798.50. |

请记住,您的借记(左侧)应等于您的信用(右侧)。如果他们不平衡,请仔细检查您的总计并寻找会计错误。

日记入场#2

当您为员工提供薪水时,制定第二期日记帐分录。当您支付员工时,您不再欠工资,因此您的负债减少。而且,您的现金会降低,因为您支付了员工。

因为这是一个责任,通过借记表来减少您的工资单应付账户。并且,减少您的现金账户(资产)以信贷。

| 日期 | 帐户 | 借方 | 信用 |

|---|---|---|---|

| XX/XX/XXXX | 薪资应付 | 798.50. | |

| 现金 | 798.50. |

日记帐#3

Eventually, you need to pay employer taxes and remit withheld taxes. This is where a third accounting entry for payroll comes in.

Reverse the payable entries with a debit and decrease your Cash account with a credit.

The amount you credit your cash account is the total amount you must remit for federal and state taxes.

| 日期 | 帐户 | 借方 | 信用 |

|---|---|---|---|

| XX/XX/XXXX | Employee FICA Tax Payable | 76.50. | |

| Employer FICA Tax Payable | 76.50. | ||

| Federal Income Tax Payable | 70 | ||

| 国家所得税应付 | 30 | ||

| 联邦失业率应付 | 25 | ||

| 国家失业率应付 | 20 | ||

| 现金 | 298 |

工资单会计不一定是复杂的。通过将您的书籍简化与爱国者的易于使用和价格实惠,简化您记录工资交易,收入和费用的方式vwin.com 软件。你在等什么?今天免费尝试!

This article has been updated from its original publication date of June 1, 2017.

This is not intended as legal advice; for more information, please点击这里。